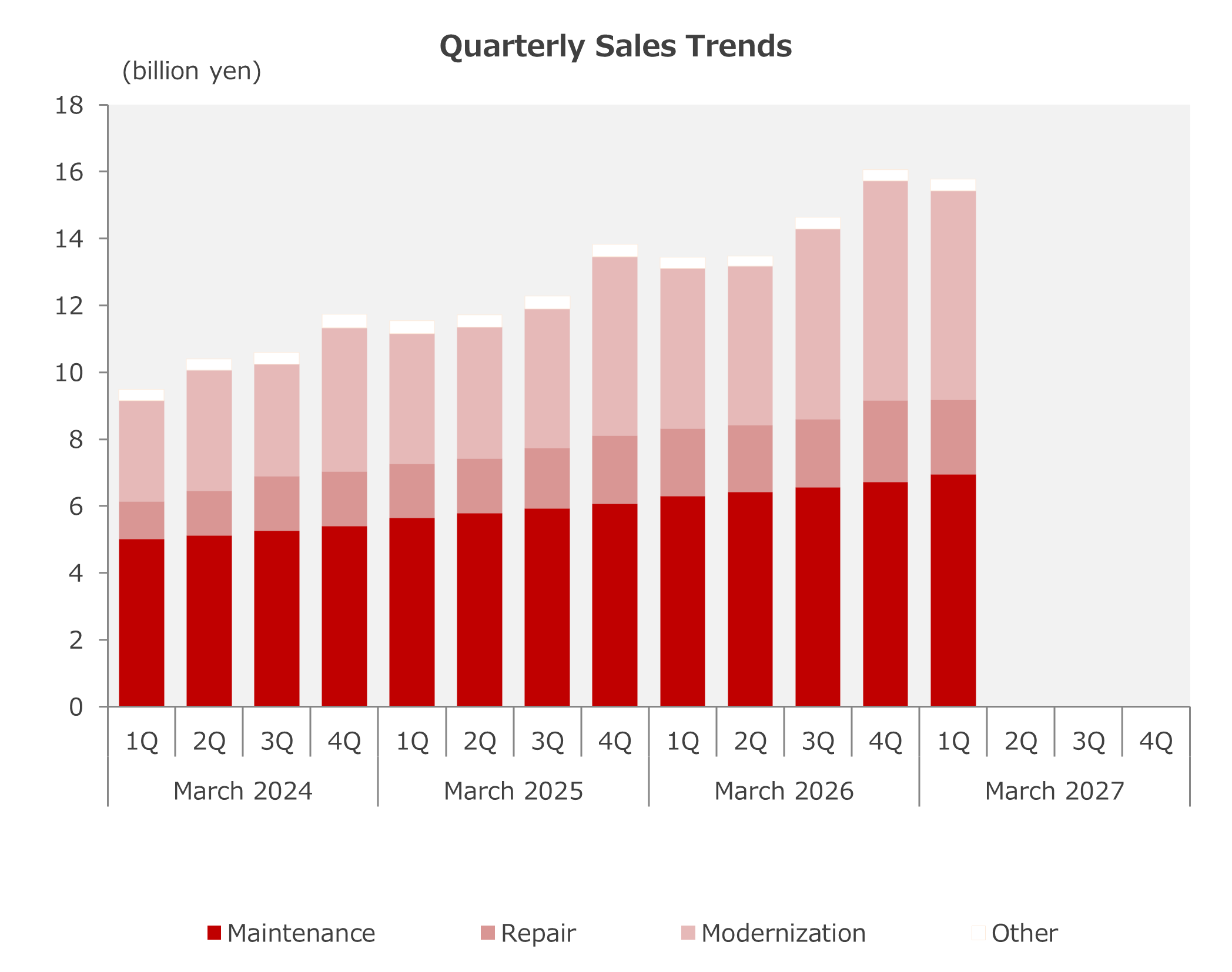

- Although modernization accounting for nearly 40% of sales, the gross profit margin remained at a high level, driven by a significant increase in unit prices for modernization and continued productivity gains resulting from an increase in the number of maintenance contracts numbers.

- Efforts to control SG&A spending also proved effective, with the SG&A ratio falling to 19.5%. Operating profits increased by 21.5% YoY, outpacing the sales growth. The operating profit margin before goodwill amortization improved by 0.6 percentage points YoY to 19.7%.

(millions of yen, yen, %)

|

3 months ended |

3 months ended |

YoY change |

||||

|

June 2025 |

June 2026 |

|||||

|

Amount |

% of sales |

Amount |

% of sales |

Amount |

% |

|

|

Net sales |

13,433 |

100.0 |

15,778 |

100.0 |

2,345 |

17.5 |

|

Operating profit |

2,505 |

18.6 |

3,044 |

19.3 |

538 |

21.5 |

|

Ordinary profit |

2,513 |

18.7 |

3,024 |

19.2 |

511 |

20.3 |

|

Profit attributable to owners of parent |

1,608 |

12.0 |

1,924 |

12.2 |

315 |

19.6 |

|

(Depreciation) |

355 |

2.6 |

426 |

2.7 |

71 |

20.0 |

|

(Amortization of goodwill) |

67 |

0.5 |

69 |

0.4 |

2 |

3.3 |

|

OP before amortization |

2,572 |

19.1 |

3,113 |

19.7 |

541 |

21.0 |

|

EPS* |

9.03 |

-- |

10.76 |

-- |

1.73 |

19.2 |

*The Company conducted a two-for-one stock split of ordinary shares on October 1, 2025. Earnings per share is calculated assuming that the stock split was conducted at the beginning of the previous fiscal year.

- Net sales from maintenance and repair services showed stable growth in line with the increase in the number of maintenance contracts.

- Modernization saw growth in both the number of units and the average unit price, and net sales rising significantly by 30.4% YoY.

- In other sales overseas operations returned to an upward trend.

(millions of yen, yen, %)

|

3 months ended |

3 months ended |

YoY change |

||||

|

June 2025 |

June 2026 |

|||||

|

Amount |

% of sales |

Amount |

% of sales |

Amount |

% |

|

|

Maintenance & Repair |

8,315 |

61.9 |

9,186 |

58.2 |

870 |

10.5 |

|

Modernization |

4,791 |

35.7 |

6,246 |

39.6 |

1,454 |

30.4 |

|

Other |

326 |

2.4 |

345 |

2.2 |

19 |

6.0 |

|

Total |

13,433 |

100.0 |

15,778 |

100.0 |

2,345 |

17.5 |

- The number of domestic maintenance contracts has exceeded 130,000 units. Net increase of 4,310 units matched that of the same period last year. Despite some volatility due to a concentration of expiring tender contracts, the number of new contracts exceeded the previous year’s level thanks to strengthened sales efforts.

- The number of modernization shipments increased from 620 units to 700 units compared to the same period last year. Large-scale projects, escalators, and a new installation project also contributed, leading to a significant increase in the average unit price.

- On June 1, the Miyazaki service office was opened, bringing the total number of locations to 158. We now have presence in all prefectures.

- The number of employees increased by 157 from the end of the previous fiscal year. In addition to recruiting new graduates, the company continued to actively hire mid-career personnel, strengthening the organization as a whole to support business expansion, including both technical and sales personnel.

(units,person)

|

FY Ended March 2023 |

FY Ended March 2024 |

FY Ended March 2025 |

FY Ended March 2025 |

3 months ended June 2026 |

||

|

Actual |

Actual |

Actual |

Actual |

Actual |

(Change YtD) |

|

|

Maintenance contracts |

88,630 |

100,230 |

113,520 |

113,520 |

131,150 |

+ 4,310 |

|

Modernization (cumlative) |

1,530 |

1,930 |

2,230 |

2,230 |

700 |

+ 80 |

|

Parking equipment (No. of pallets) |

22,050 |

24,660 |

26,740 |

26,740 |

28,790 |

+ 1,140 |

|

No. of offices |

132 |

138 |

148 |

148 |

158 |

+ 3 |

|

No. of employees Technical personnel Sales personnel |

1,766 1,096 218 |

1,868 1,159 248 |

2,028 1,271 272 |

2,028 1,271 272 |

2,443 1,578 315 |

+ 157 + 126 + 10 |