- In maintenance and repair, net growth in maintenance contracts is expected to continue. In modernization, growth in shipments and unit prices is expected.

- In addition to productivity improvements due to the increase in the number of contracts, the company expects to continue to control SG&A expenses and achieve an operating profit margin before amortization of over 20%. As a result, both sales and profits are expected to reach new highs.

(millions of yen, %)

|

March 2026 |

March 2027 Forecast |

||||

|

Amount |

% of sales |

Amount |

% of sales |

YoY |

|

|

Net sales |

57,601 |

65,000 |

112.8 |

||

|

Operating profit |

11,010 |

19.1 |

13,000 |

20.0 |

118.1 |

|

Ordinary profit |

11,006 |

19.1 |

13,000 |

20.0 |

118.1 |

|

Profit attributable to owners of parent |

7,319 |

12.7 |

8,200 |

12.6 |

112.0 |

|

(Depreciation) |

1,587 |

2.8 |

1,800 |

2.8 |

113.4 |

|

(Amortization of goodwill) |

291 |

0.5 |

277 |

0.4 |

95.1 |

|

OP before amortization |

11,301 |

19.6 |

13,277 |

20.4 |

117.5 |

(millions of yen, %)

|

March 2026 |

March 2027 Forecast |

||||

|

Amount |

% of sales |

Amount |

% of sales |

YoY |

|

|

Maintenance & repair services |

34,499 |

59.9 |

37,800 |

58.2 |

109.6 |

|

Modernization services |

21,801 |

37.8 |

25,900 |

39.8 |

118.8 |

|

Other |

1,300 |

2.3 |

1,300 |

2.0 |

99.9 |

|

Net Sales |

57,601 |

100.0 |

65,000 |

100.0 |

112.8 |

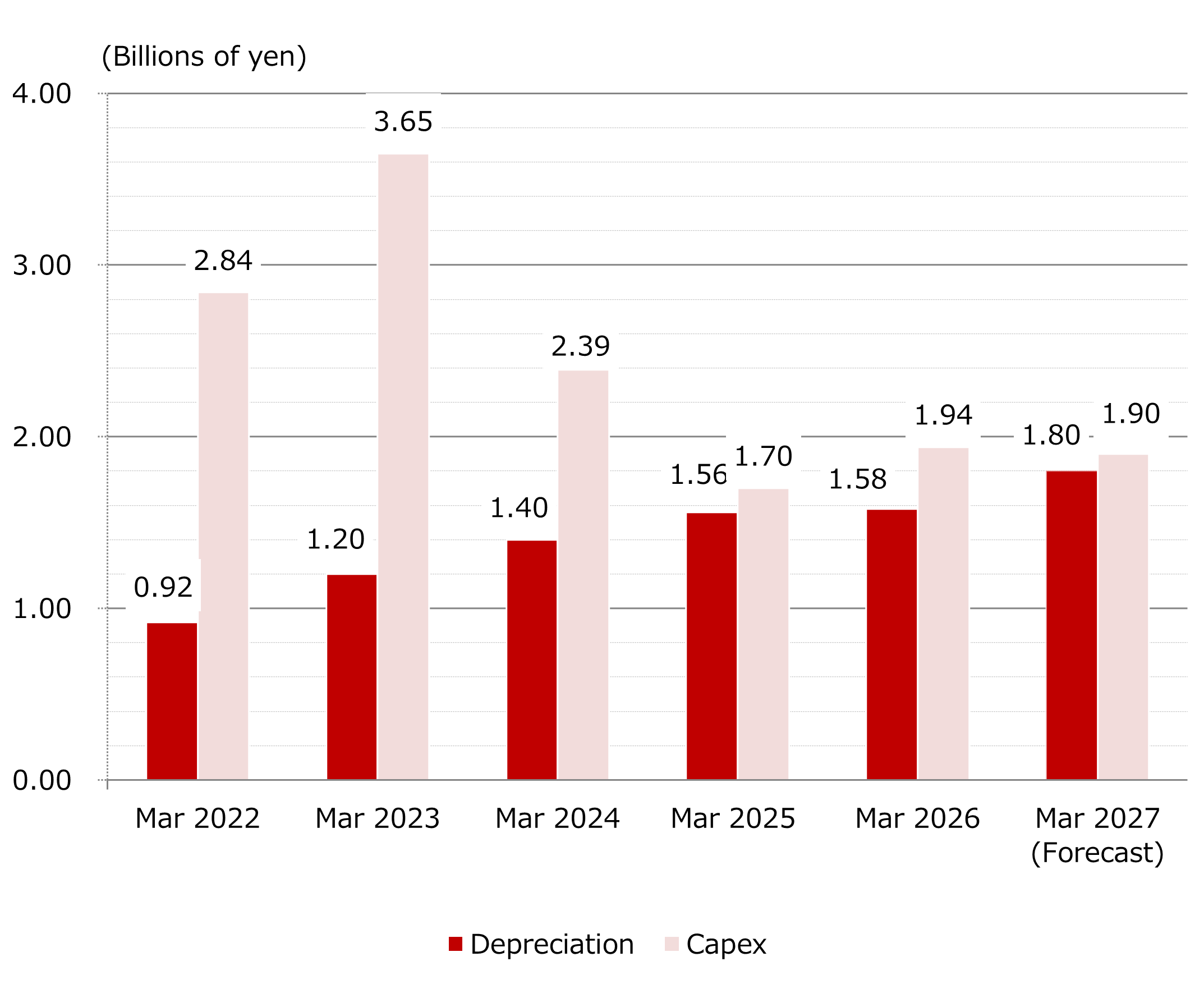

(billions of yen)

|

FY2026 (Actual) |

FY2027 (Forecast) |

Items |

|

|

Capital Expenditures |

1.94 |

1.90 |

Investments related to PRIME, a remote inspection service, etc. |

|

Depreciation |

1.58 |

1.80 |

Trends in Capital Expenditures and Depreciation

Disclosed on May 14, 2026